PA Cannot Tax Its Way into an Innovation Economy

Pennsylvania says it wants the jobs of the future. Gov. Josh Shapiro has made attracting life sciences, advanced manufacturing, robotics, technology, and research-driven employers a centerpiece of his economic development message. At BIO 2025, the Administration touted Pennsylvania’s life sciences sector, a proposed $50 million PA Innovation program, and the state’s effort to attract new businesses by leveraging research institutions, workforce assets, and industry clusters.

That is the right aspiration, but Pennsylvania’s tax policy is moving in the opposite direction.

In the most recent budget, Harrisburg chose to decouple Pennsylvania’s Corporate Net Income Tax from key federal expensing provisions adopted under the federal One Big Beautiful Bill Act, H.R. 1. The Department of Revenue states plainly that Act 45 of 2025 decouples Pennsylvania CNIT from certain federal provisions in H.R. 1, including changes affecting research and experimental expenditures and other business investment rules.

Put simply: Washington moved to make it easier for companies to invest in research, equipment, production capacity, and innovation; Harrisburg chose to make those investments more expensive in Pennsylvania.

This decision is far beyond just a small technical matter for accountants … it’s a competitiveness differentiator.

Full expensing is based on a simple principle: when a business puts money back into research, machinery, technology, facilities, or production improvements, government should not treat those dollars as if they were ordinary profits sitting idle. Expensing allows companies to recover investment costs immediately rather than slowly over time. That improves cash flow, lowers the after-tax cost of investment, and makes it easier for businesses to say yes to projects that create jobs, raise productivity, and strengthen supply chains. It was a key provision missing from the 2017 Tax Cuts and Jobs Act, but was one of the key attributes of H.R. 1.

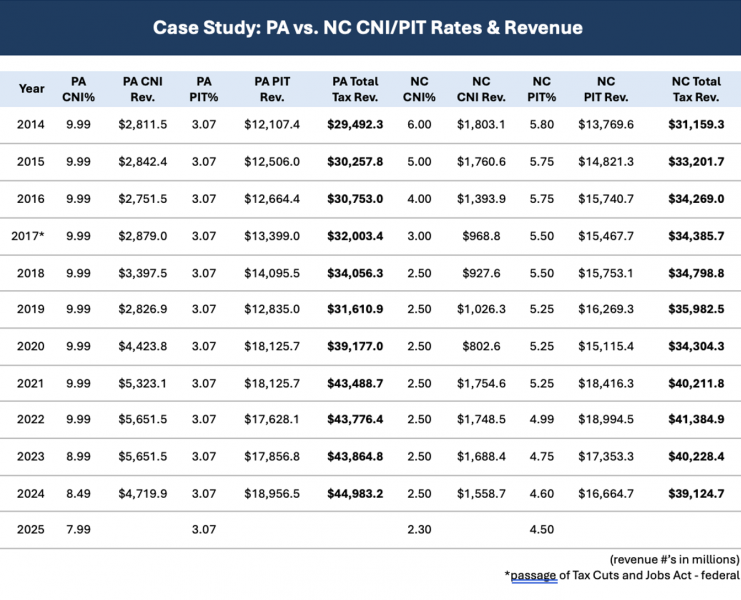

Tax rates/treatments and tax returns are two different things. And the evidence on this statement is not abstract. PMA’s comparison of Pennsylvania and North Carolina shows the competitiveness lesson clearly. In 2014, North Carolina’s Corporate Net Income Tax rate was 6.0%, and its Personal Income Tax rate was 5.8 percent. By 2024, those rates had fallen to 2.5% and 4.6%, respectively. Yet, North Carolina’s combined CNI and PIT revenue grew from $31.2 billion in 2014 to $39.1 billion in 2024. Over that same period, Pennsylvania kept its PIT rate flat at 3.07% and only began reducing its CNI rate recently, while total tax revenue also grew — but without the same aggressive competitiveness signal. The lesson is that lower, more competitive tax rates do not mean economic surrender but instead coincide with stronger investment, broader growth, and more durable revenues promoting long-term state fiscal stability.

Tax competitiveness influences where boardrooms locate plants, labs, pilot lines, production expansions, and technology teams. Pennsylvania cannot tell high-tech manufacturers, pharmaceutical innovators, software firms, robotics companies, energy producers, and advanced materials businesses that we want their jobs while also being an outlier among states by imposing a state tax penalty on the very investments those jobs require.

The contradiction is especially damaging for research and development. PMA’s recent economic analysis found that Pennsylvania directly employs 185,720 professionals in R&D, supporting 427,997 total direct, indirect, and induced jobs, $41.9 billion in labor income, $59.9 billion in gross state product, and $107.8 billion in total economic output. These are not speculative jobs. They are already part of Pennsylvania’s economic foundation.

They are also exactly the jobs the Commonwealth says it wants more of.

The Governor touts Pennsylvania’s life sciences sector as employing more than 100,000 people across nearly 3,100 companies and research institutions. The Administration also says Pennsylvania researchers and companies secured more than 10,700 life sciences patents over five years, the fourth-highest total in the nation, and that nearly 60 percent of projected life sciences job growth over the next decade is expected to be concentrated in research and development.

Those facts should lead to one obvious conclusion: Pennsylvania should not tax research-intensive investment more harshly than competitor states.

Yet, that is precisely what decoupling does. It preserves state revenue on paper by increasing the tax burden on companies making the kinds of investments Pennsylvania claims to value most. The Senate Appropriations Committee fiscal note stated that decoupling would prevent the Commonwealth from losing more than $1.1 billion in FY 2025-26. But that framing misses the broader economic question. The issue is not whether Harrisburg can collect more money in the short term by denying businesses full expensing. Of course it can. The issue is what Pennsylvania loses when projects are delayed, scaled back, automated elsewhere, or never brought here in the first place.

That loss is harder to quantify. It appears as the factory that is not modernized, the production line that is not expanded, the research team hired in another state, the supplier contract that never reaches a Pennsylvania company, the patent commercialized in a competitor state, or the family-sustaining paycheck that never shows up for a Pennsylvania household.

Pennsylvania already knows how important these projects are. The Administration has celebrated major life sciences and manufacturing investments and has emphasized its desire to win more of them. It has highlighted more than $25 billion in private-sector investments since taking office and pointed to expanded operations by life sciences firms bringing new jobs and R&D investment into the Commonwealth.

Those wins should be reinforced, not undermined.

The Commonwealth cannot build an innovation economy through press conferences while weakening the tax treatment of innovation behind the scenes. Economic development grants, ribbon cuttings, and targeted programs may help at the margins, but the tax code sends a broader and more lasting signal. A state that punishes investment is telling site selectors to look elsewhere.

That is especially dangerous because Pennsylvania’s competitors are not standing still. PMA’s prior analysis found that Pennsylvania will be an outlier among competitor states, with only Rhode Island, Connecticut, and Michigan adopting R&D expensing treatment similar to Pennsylvania, while states including Tennessee, Georgia, and New Jersey have acted in recent years to allow full expensing even when the federal government did not.

This should be a bipartisan concern. Expensing is not a special carveout for one favored industry. It is a neutral tax policy that applies to the building blocks of growth: research, equipment, productivity, and capital formation. It helps manufacturers improve processes, pharmaceutical companies develop treatments, software firms build platforms, energy producers modernize operations, and startups turn ideas into products.

If Pennsylvania wants to compete for premium jobs in the modern economy, it must align its tax code with that goal. The General Assembly should reverse course and restore Pennsylvania’s conformity with federal expensing for research and business investment. Doing so would strengthen the Commonwealth’s competitiveness, support employers already investing here, and send a clear message that Pennsylvania is serious about building an innovation economy.

Pennsylvania has the workforce, universities, manufacturers, research institutions, energy resources, and geographic advantages to win. But other states want the same jobs. If Harrisburg makes investment more expensive here, employers will not wait for Pennsylvania to figure it out. They will simply go where the tax code rewards growth rather than punishes it.